Back محاسبة الاستدامة Arabic Yhteiskunnallinen laskentatoimi Finnish Normes comptables de durabilité French Rachunkowość zrównoważona Polish د پايښت محاسبه Pashto/Pushto

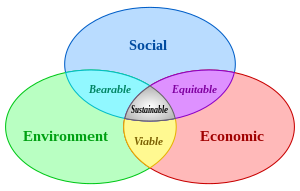

Sustainability accounting (also known as social accounting, social and environmental accounting, corporate social reporting, corporate social responsibility reporting, or non-financial reporting) originated in the 1970s[1] and is considered a subcategory of financial accounting that focuses on the disclosure of non-financial information about a firm's performance to external stakeholders, such as capital holders, creditors, and other authorities. Sustainability accounting represents the activities that have a direct impact on society, environment, and economic performance of an organisation.[2] Sustainability accounting in managerial accounting contrasts with financial accounting in that managerial accounting is used for internal decision making and the creation of new policies that will have an effect on the organisation's performance at economic, ecological, and social (known as the triple bottom line or Triple-P's; People, Planet, Profit) level. Sustainability accounting is often used to generate value creation within an organisation.[3]

Sustainability accounting is a tool used by organisations to become more sustainable. The most known widely used measurements are the Corporate Sustainability Reporting (CSR) and triple bottom line accounting. These recognise the role of financial information and shows how traditional accounting is extended by improving transparency and accountability by reporting on the Triple-P's.

As a result of triple bottom level reporting, and in order to render and guarantee consistency in social and environmental information, the GRI (Global Reporting Initiative) was established with the goal to provide guidelines to organisations reporting on sustainability. In some countries, guidelines were developed to complement the GRI. The GRI states that "reporting on economic, environmental and social performance by all organizations is as routine and comparable as financial reporting".[4]

In order to help finance teams and accountants embed sustainability into their accounting, King Charles III, then Prince of Wales, set up his Accounting for Sustainability project (A4S) in 2004.[5]

- ^ Hardyment, R. (2024) Measuring Good Business: Making Sense of Environmental, Social and Governance (ESG) Data. Abingdon, Oxon: Routledge. ISBN 9781032601199

- ^ "15 Types of Accounting to Know in 2022". netsuite.com.

- ^ Perrini, Francesco; Tencati, Antonio (September 2006). "Sustainability and stakeholder management: the need for new corporate performance evaluation and reporting systems". Business Strategy and the Environment. 15 (5): 296–308. doi:10.1002/bse.538.

- ^ "Global Reporting Initiative". Globalreporting.org. Retrieved 2013-09-24.

- ^ Accounting for Sustainability. "Accounting for Sustainability". Accounting for Sustainability. Retrieved 19 February 2016.

- ^ Adams, W. M. (2006)."The Future of Sustainability: Re-thinking Environment and Development in the Twenty-first Century." Report of the IUCN Renowned Thinkers Meeting, 29–31 January 2006. Retrieved on: 2009-02-16.

© MMXXIII Rich X Search. We shall prevail. All rights reserved. Rich X Search